Education · Risk Management · 9 min read

Open any trading book and the advice on position sizing splits into two camps. Camp one says “risk a fixed percentage of your account on every trade”. Camp two says “risk a fixed dollar amount”. Both have advocates with track records. Both sound reasonable. But under different account conditions, one of them will quietly destroy you while the other lets you compound.

The right answer is not “always pick one.” The right answer is knowing which method matches your account size, your strategy, and the phase of your trading career you are in.

The Short Answer

Fixed % is mathematically superior for compounding accounts above $10k. Fixed $ is more practical for very small accounts and for prop firm challenges with strict daily loss caps. Most traders should use fixed % with a hard dollar ceiling — the best of both worlds.

How Each Method Actually Works

Before debating which is better, let us define exactly what each one does on a real trade.

Fixed Percentage Risk

You decide on a percent of your account to risk per trade — say 1%. The actual dollar risk recalculates with every change in account balance. After winners, your dollar risk grows. After losers, it shrinks.

Account: $10,000 · 1% risk = $100 per trade

Account grows to $15,000 · 1% risk = $150 per trade

Account drops to $8,000 · 1% risk = $80 per trade

Fixed Dollar Risk

You decide on an exact dollar amount to risk per trade — say $100 — and you keep that amount constant regardless of what happens to the account.

Account: $10,000 · fixed $100 = 1.0% risk

Account grows to $15,000 · fixed $100 = 0.67% risk

Account drops to $8,000 · fixed $100 = 1.25% risk

Notice the asymmetry: with fixed $, your effective risk percentage grows when the account shrinks. This is the core danger of fixed dollar sizing — and the core advantage of fixed percentage sizing.

The Compounding Argument for Fixed %

Fixed % wins the math contest hands down. Imagine two traders with $10,000 accounts, both running a strategy that produces 100 trades per year with a 60% win rate and 1:1 R:R. Both risk $100 per trade in absolute terms at the start of year one.

After year one, both accounts are at $12,000 (60 wins minus 40 losses, net +$2,000). Now what happens in year two?

YEAR 2 — STARTING AT $12,000

Trader A (1% fixed) → risks $120/trade → ends year at $14,400

Trader B ($100 fixed) → risks $100/trade → ends year at $14,000

A 2.8% advantage in year two. Repeat this for ten years and Trader A is significantly ahead — not because their strategy is better, but because their risk grew with their winnings. Compounding only works if your bet size scales with your bankroll.

The opposite case is more painful. If both traders have a bad year and end down at $8,000, Trader A automatically risks less ($80/trade) for year two — which protects them. Trader B keeps risking $100/trade, which is now 1.25% of a smaller account. If the bad year continues, Trader B accelerates toward zero while Trader A decelerates.

When Fixed Dollar Actually Wins

If fixed % is mathematically dominant, why does anyone still use fixed $? Because in three specific situations it is genuinely the better choice.

1. Very Small Accounts

On a $500 account, 1% risk is $5. Many brokers have minimum lot sizes that make $5 risk impossible to achieve precisely — you end up either over-risking (the next-step-up lot size risks $8 or $12) or unable to take the trade at all. Fixed dollar sizing lets you set a workable risk amount that matches what your broker will actually accept.

2. Prop Firm Challenges with Daily Loss Caps

Most prop firms (FTMO, MyForexFunds, etc.) impose a hard daily loss limit — often 4% or 5% of starting balance. With fixed % sizing, your dollar risk per trade compounds along with profits during a winning streak inside the day, which can push you over the daily cap faster than expected. Fixed dollar sizing keeps your daily exposure mathematically capped: 4 trades at $200 risk = $800 max daily loss, locked.

3. Strategies with Variable Win Quality

If your strategy has clearly defined “A-grade” and “B-grade” setups (think: trades meeting all your criteria vs trades meeting most), fixed dollar sizing per grade is cleaner than constantly recalculating percentages. You might risk $200 on every A-setup and $100 on every B-setup, regardless of account size. This makes performance review much easier — you can immediately see which grade is actually profitable.

Reality Check

Fixed dollar is also psychologically easier when the account is in drawdown. It is harder to take a trade when “1% of my account” keeps getting smaller and feels like surrender. A constant dollar amount feels more like business-as-usual.

The Hybrid Approach Most Traders Should Use

In practice, the smartest setup combines both. Here is the rule that experienced traders converge on after a few years:

Risk = MIN(account x 1%, fixed $ ceiling)

Translation: risk 1% of your account per trade, but never more than a hard dollar ceiling you set in advance. For example: 1% of account, capped at $500 per trade.

Why this works:

- Below the ceiling, you get the compounding benefit of fixed % — your risk grows with the account, your wins grow proportionally.

- Above the ceiling, your absolute dollar risk stops growing. This protects you from a single trade becoming psychologically too large to manage rationally — a real problem once accounts cross six figures.

- In drawdown, fixed % automatically reduces your absolute risk — so you decelerate naturally when things go wrong.

Most traders start with pure fixed % (1% or 0.5%) and add the dollar ceiling later when their account grows large enough that risking the full % per trade starts feeling uncomfortable.

The Mistake That Kills Both Methods

Whether you use fixed % or fixed $, both methods break the moment you start trading instruments where your lot size calculation is silently wrong.

A trader can set their system to “1% per trade” and feel disciplined. But if they switch from EURUSD to gold and apply the same lot size mental math, they may actually be risking 5% or 10% — and they will not notice until the equity curve confirms it. The same problem hits fixed dollar traders: “I always risk $100” sounds disciplined, but if your gold trade is actually risking $700 because the tick value math went wrong, the discipline is illusion.

This is why both methods only work when paired with automated lot calculation that reads the instrument’s real Tick Size and Tick Value. Without that, you are picking between two methods that will both lie to you about how much you are actually risking.

Common Trap

Switching between fixed % and fixed $ midway through a losing streak. This is almost always emotional, not strategic — traders move to fixed $ during drawdowns to “stop the bleeding from getting smaller” and then back to fixed % during recoveries. Pick one method, write it down, and only change it after a 100-trade review — never mid-streak.

Choosing What Fits Your Account Today

A practical decision tree for traders who want a clear answer right now:

- Account under $1,000: Fixed dollar — broker lot minimums make % sizing impractical.

- Account $1,000-$10,000: Fixed % at 0.5%-1% — small enough to compound meaningfully, large enough to absorb a 10-trade losing streak.

- Account $10,000-$100,000: Fixed % at 1% — this is the sweet spot where compounding compounds and drawdown protection kicks in automatically.

- Account above $100,000: Fixed % with dollar ceiling — set the ceiling at whatever absolute loss feels manageable per trade.

- Prop firm challenges: Fixed dollar at the level that keeps your worst-day-loss safely below the daily cap, regardless of how many trades you take.

Making the Method Match the Math

Whichever method you pick, the calculation needs to happen automatically before every single trade. Manual recalculation is where the system breaks — markets move fast, you skip a step, and the next thing you know your “1%” trade is actually risking 4% because you eyeballed the lot size.

A proper trading dashboard handles this in real time: you set your method (% or $), enter your stop loss, and the platform reads the instrument’s real Tick Value to calculate the correct lot size instantly. No mental gymnastics, no broker-specific lookup tables, no silent over-risking on gold and indices.

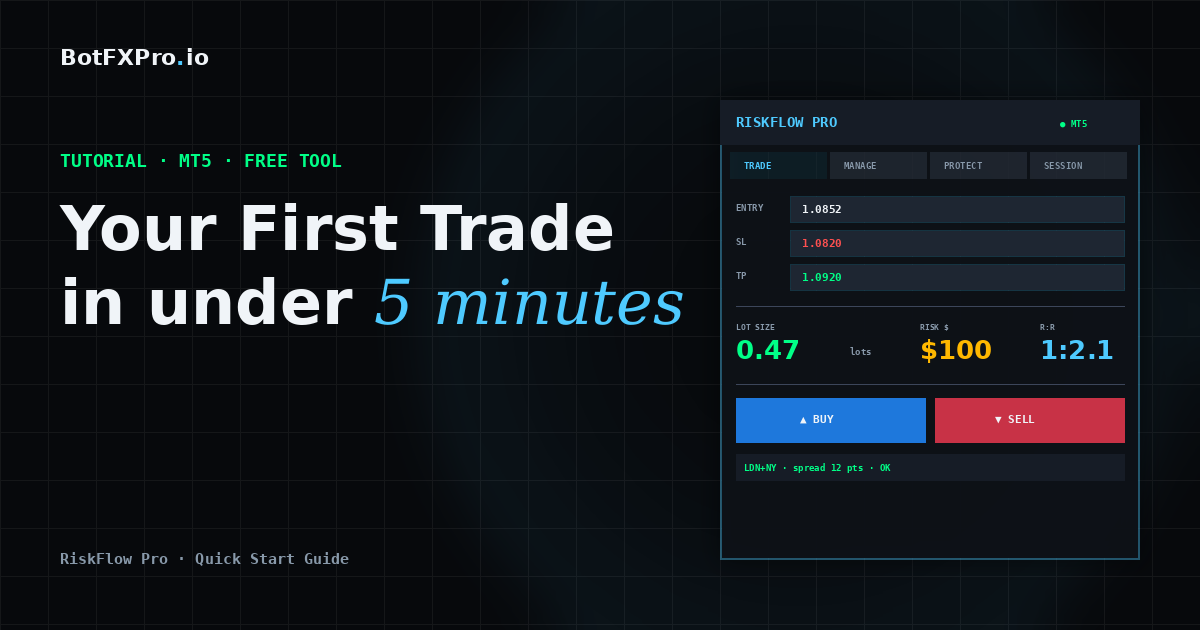

RiskFlow Pro supports four risk modes — % Balance, % Equity, Fixed $, and % Free Margin — and switches between them with one click. Whichever method you decide fits your account today, you can run it without recalculating anything by hand.

For a deeper look at the four risk modes, the daily drawdown protection, and the multi-level partial close that pairs naturally with fixed % sizing, the Advanced Features guide walks through each setting in detail with real examples — especially useful if you are running prop firm challenges where the choice between % and $ sizing has direct rule-compliance implications.

Key Takeaways

- Fixed % wins the long-term compounding contest — your bet size scales with the bankroll, both up and down.

- Fixed $ wins for very small accounts, prop firm challenges with daily caps, and graded-setup strategies.

- The hybrid “fixed % capped at a dollar ceiling” gives most traders the best of both above $50k.

- Both methods break silently when applied to instruments where lot sizing math is wrong — gold, oil, indices, CFDs.

- Never switch methods mid-streak. Lock the choice in writing and review only every 100 trades.

Get RiskFlow Pro

Switch between four risk modes with one click.

% Balance, % Equity, Fixed $, % Free Margin — all calculated correctly on any instrument, any broker.

For prop firm setups and the four risk modes in detail, see the Advanced Features Guide.